#8: Strategising Differently; Stanford on AI; Tech & Bank Runs; Shifting Alliances; Politics and Pro Wrestling

#8: Strategising Differently; Stanford on AI; Tech & Bank Runs; Shifting Alliances; Politics and Pro Wrestling

Happy Easter

Happy Easter to everyone. It’s a shortened newsletter this week as this is a weekend for spending time with family and feeling optimistic with the burst of spring. I thought this week would be a good time to round up a few things we’ve been reading recently.

Thanks so much for all of the comments on previous newsletters. Very much appreciated. Please do keep on sharing and subscribing. And please use the like ♡ button if you can - seemingly Substack’s algorithms love the like button!

As always, get in touch via email david@artemonstrategy.com and djskelton or artemonstrategy on Twitter.

Last week, we used the Masters golf tournament to talk about how opportunity can lie in great uncertainty. The weather gods have rather gone out of their way to prove my point. Sodden greens and falling trees have caused chaos and meant that plenty of golfers defaulted to risk management and damage limitation mode. Brooks Koepka and Jon Rahm took the bull by the horns, saw the opportunity and now seem to have the tournament to themselves. Should be compulsive viewing later today.

The Need To Strategise Differently

It was notable how JP Morgan’s Chairman and CEO used his letter to shareholders to emphasise the importance of growing uncertainty on business. He said that:

“Across the globe, 2022 was another year of significant challenges: from a terrible war in Ukraine and growing geopolitical tensions — particularly with China — to a politically divided America. Almost all nations felt the effects of global economic uncertainty… Essentially, we may be moving, as I read somewhere, from a virtuous cycle to a vicious cycle. Of course, we hope that everything turns out okay and that all of these storm clouds peacefully and painlessly dissipate – and we need to be prepared for that outcome. We also need to be prepared for a new and uncertain future.”

This uncertainty is why at Artemon we believe that Foresight capabilities are absolutely essential for any organisation. This piece in Chief Executive magazine is spot on when it talks about the need for leaders to “strategise differently” and “start planning strategically for many strategic futures”. As they argue:

Embracing the uncertainty of the post-pandemic future requires CEOs to simultaneously plan for many plausible scenarios and recovery paths (reflecting internal and external potential factors). Linking that internal and external fact base to corresponding indicators can help organizations anticipate different futures, embrace uncertainty, build strategic flexibility and analyze possible paths forward. This empowers leaders to tackle whatever comes up quickly because much of the strategizing for that possibility was done in advance. That right there? That becomes your competitive edge.

This is at the core of the service that Artemon provides. Please check out our website and get in touch to discuss more about how we can help you.

Stanford’s AI Index

Everyone’s an AI expert if you look at Linked In (or even the Twitter accounts where the crypto experts have now unsubtly rebranded themselves as AI gurus), but the folks at Stanford are the real deal and they’ve been publishing their AI Index since 2017. This year’s Index was published a few days ago and the whole 300+ page report is well worth reading in full. In case you haven’t the time today, I’ve summarised the main takeaways below:

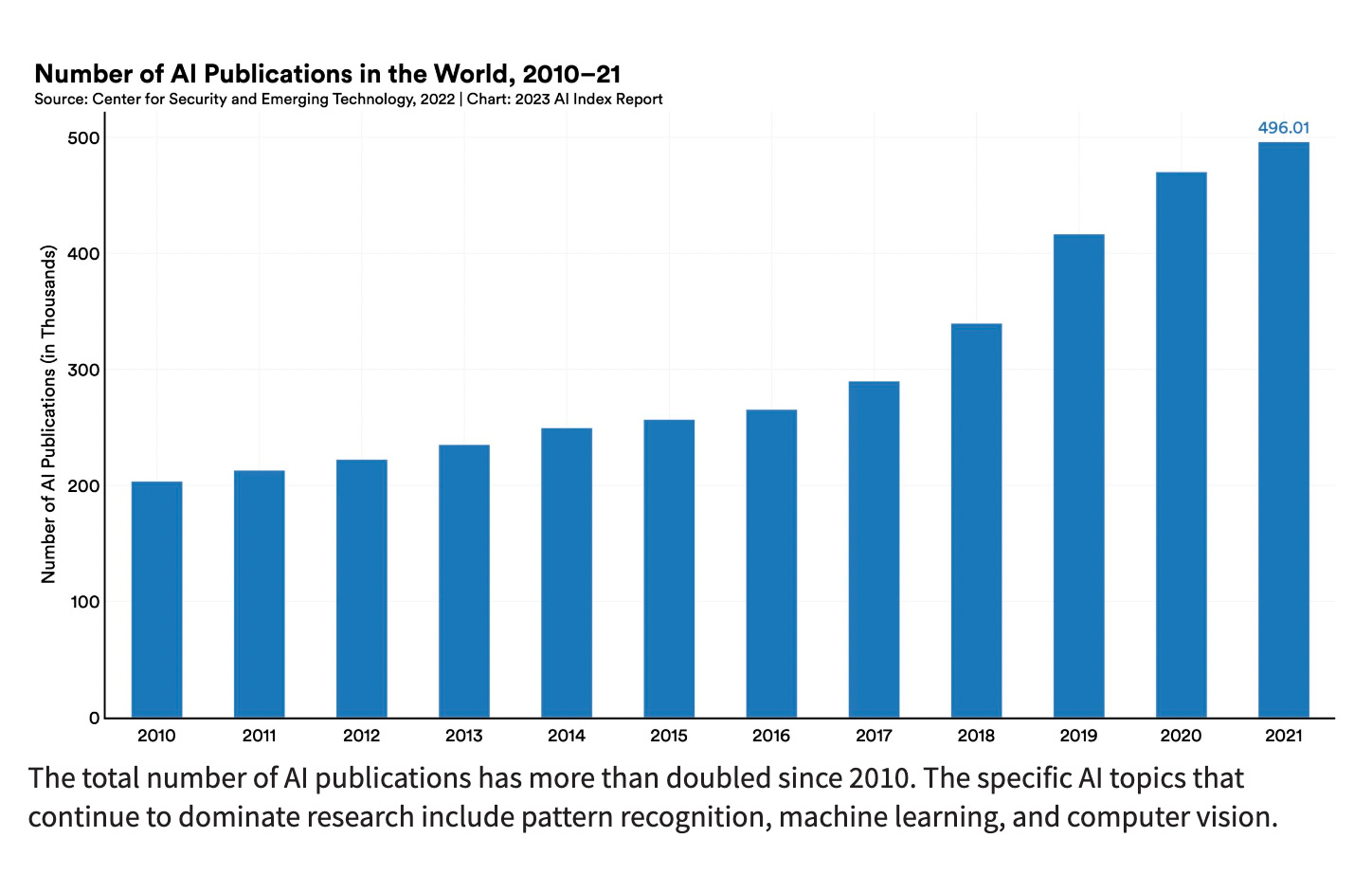

AI research continues to rise.

And the chart below was from before the surge of interest following the launch of Chat GPT.

Industry has surged ahead of academia in the production of new AI models.

Before 2014, it was academia that was largely taking the lead. The notable industry led surge started in 2018. Again, you’d expect the Chat GPT led excitement within tech to accelerate this trend.

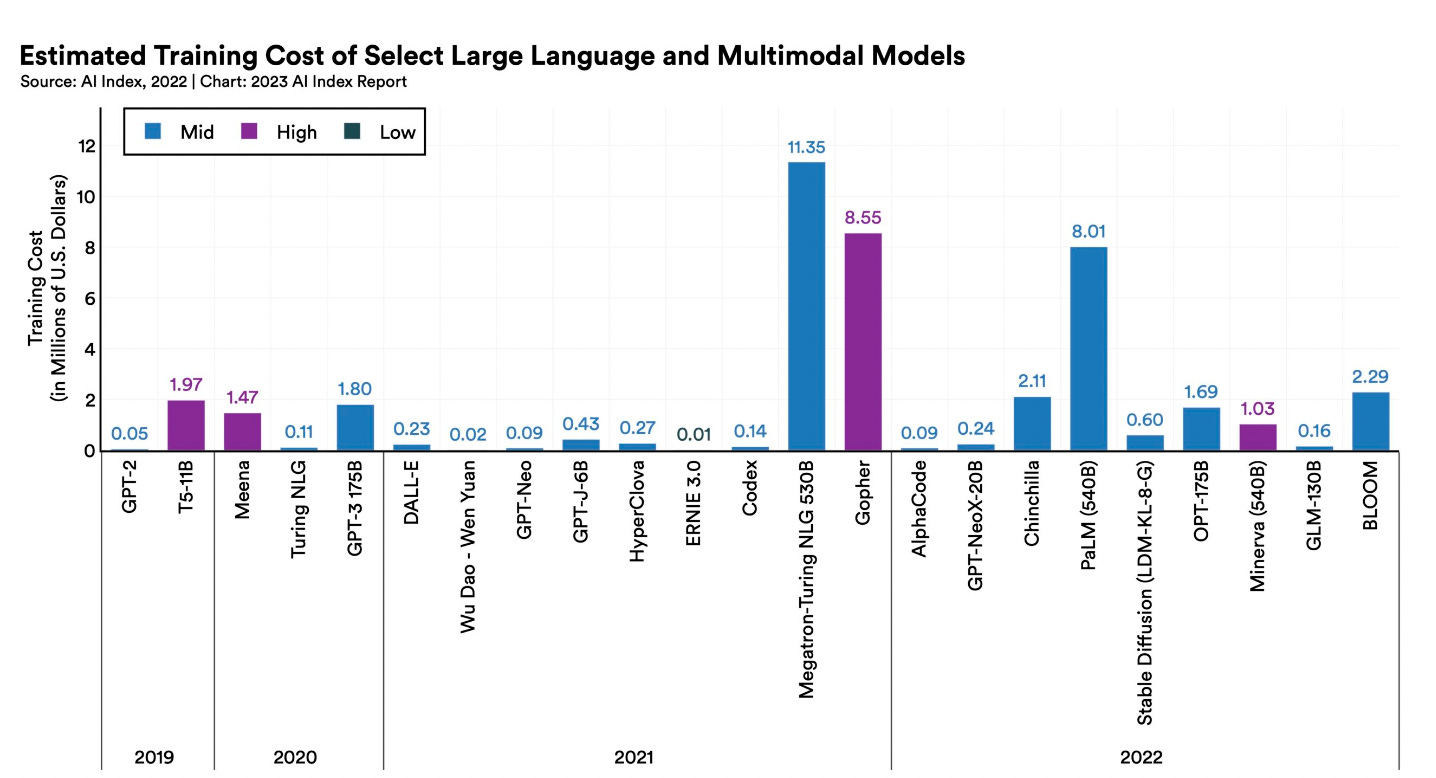

Large language models are getting bigger and more expensive

According to the report, “GPT-2, released in 2019 had 1.5 billion parameters and cost an estimated $50,000 USD to train. PaLM, one of the flagship large language models launched in 2022, had 540 billion parameters and cost an estimated $8 million USD—PaLM was around 360 times larger than GPT-2 and cost 160 times more.” It remains to be seen what this means for market concentration in emerging AI (incumbent strength versus insurgent potential) or how much investors will get nervous as tech companies bet more haevily on increasingly expensive language models.

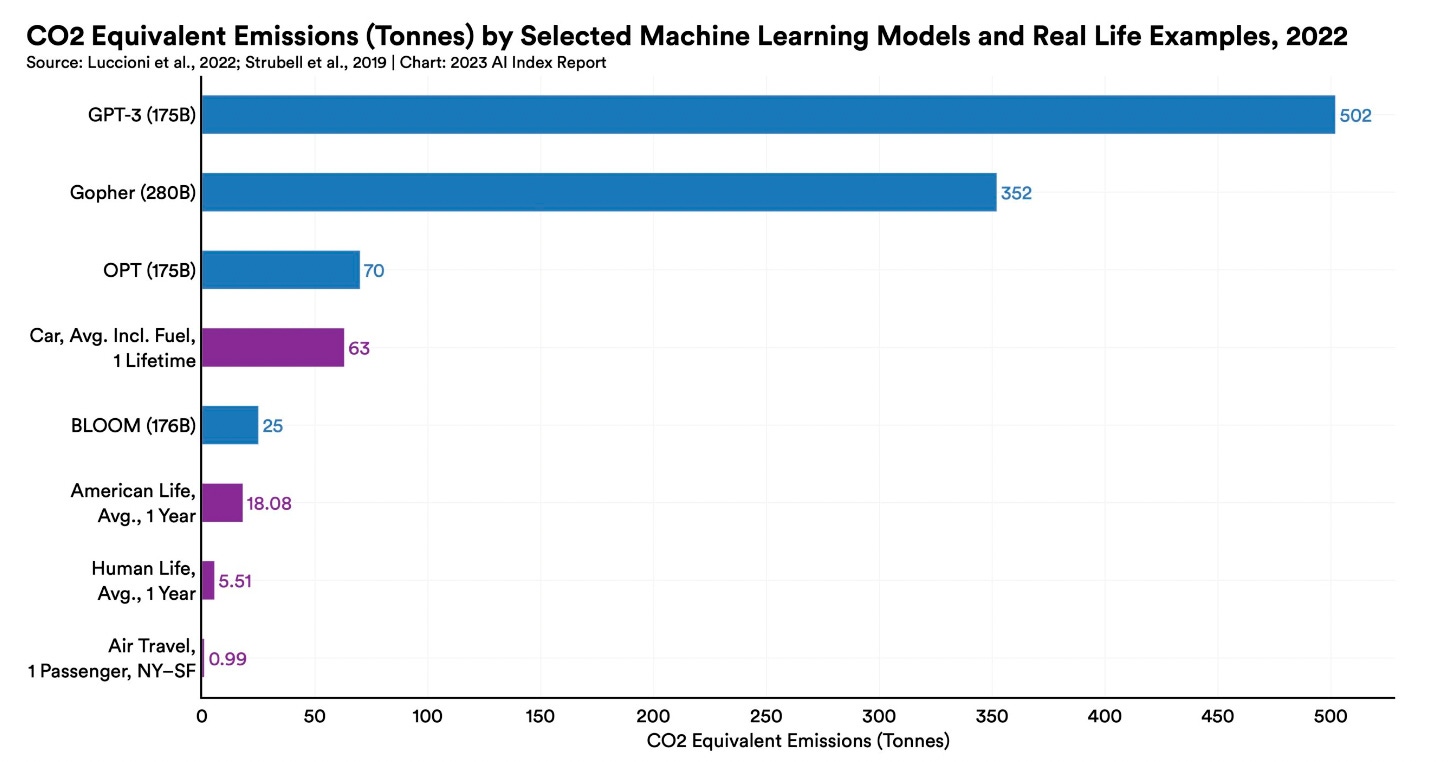

AI models use a lot of energy. Could this impact tech’s sustainability drive?

After years of tech companies investing in impressive sustainability efforts, the shift towards generative AI presents new challenges. However, there are already developments that might limit energy use from language models.

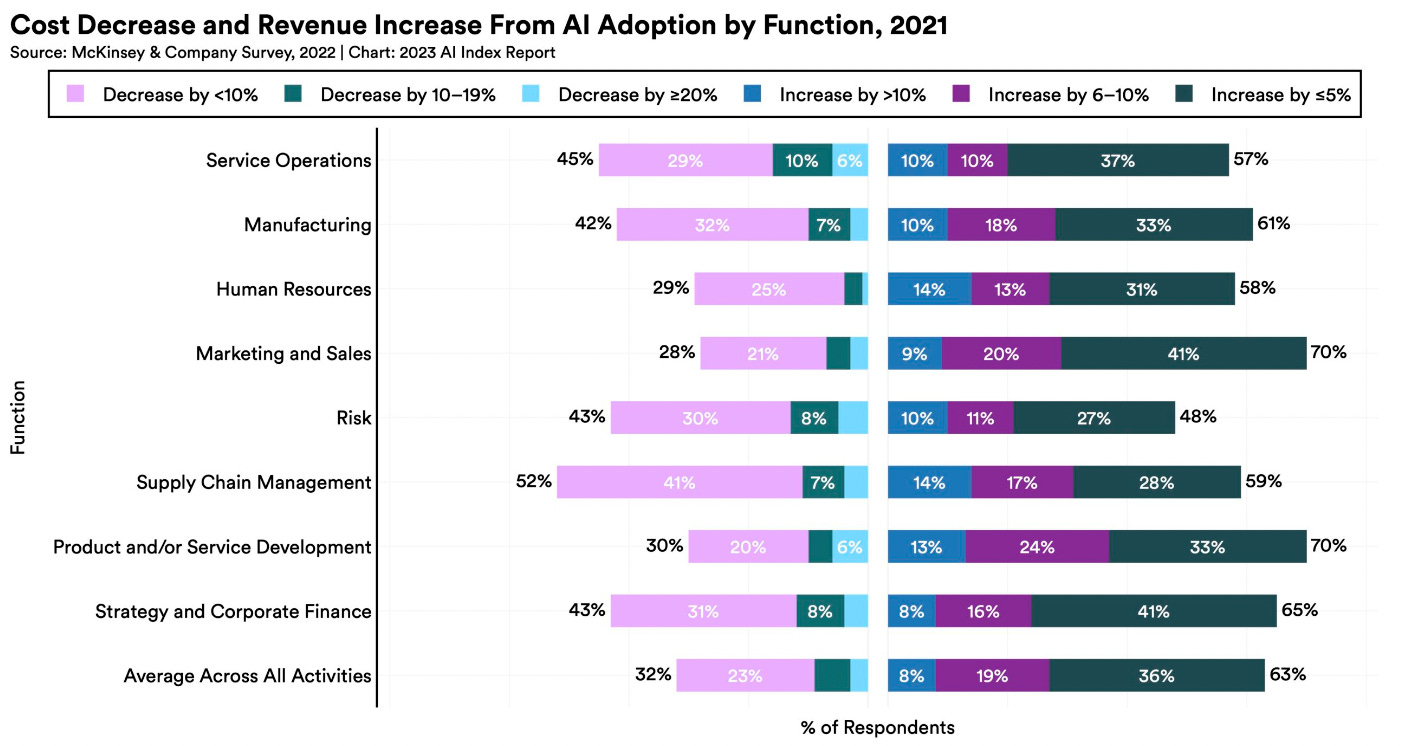

Companies that have invested in AI have already established meaningful cost decreases and revenue increases.

This illustrates the clear business rationale in properly investing in AI. As we argued in Inflection Points 6, this means that all companies need to take AI seriously and develop a comprehensive AI strategy. Maximising the benefits of AI should be a board level consideration.

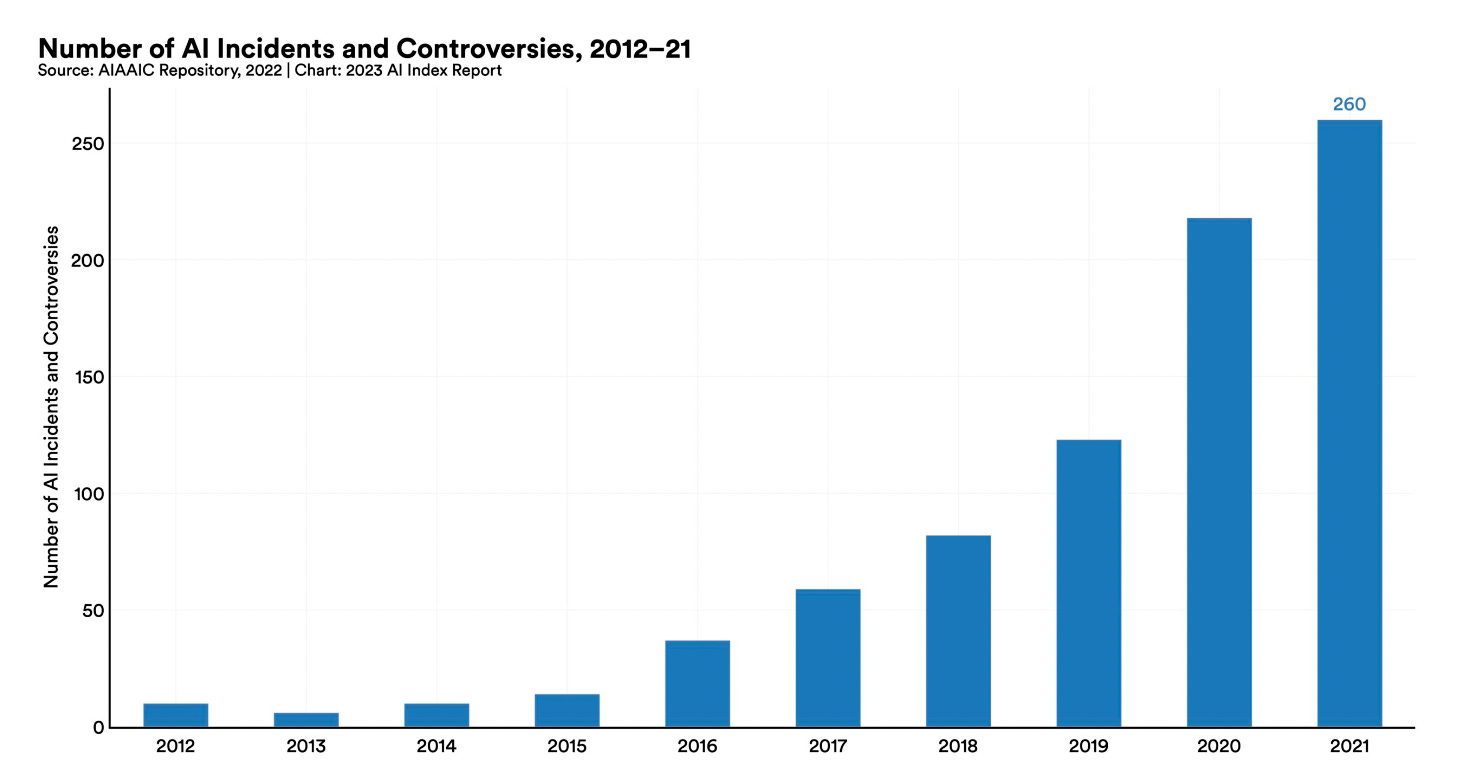

Generative AI has its issues regarding bias and fairness. Governments are moving to regulate.

The number of incidents involving misuse of AI has been increasing rapidly and governments around the world are showing an increasing interest in AI and its regulation. Notably, policymaker discussion around AI has generally avoided a regulatory kneejerk. This, from Tate Ryan-Mosley is a good primer about the issues facing regulators.

The UK government’s white paper is worth a read in itself and its focus on innovation, interoperability and international cooperation is welcome.

Slightly more surprisingly, given its shift towards hostility towards big tech, the suggestion that India has “no plans to regulate AI” is definitely a statement that might be tested by emerging events. This might, of course, be driven by a desire for a “self reliant” India to be a leader in next generation AI.

Technology and bank runs

We noted in Inflection Points 5 that the collapse of Silicon Valley bank was accelerated by what David Ulevitch described as “the first memetic, social media fueled bank run”. In The Economist, Buttonwood went into more detail about how tech breakthroughs through history, from the telegraph to the internet have led to “sudden market wobbles”.

After the fall of Silicon Valley Bank, the idea of faster bank runs is understandably causing concern among analysts and legislators. Yet the wave of new tech in the past decade and a bit is by no means the first to change behaviour. Previous examples suggest something of a pattern: innovations initially help facilitate a boom, contributing to exuberance based on a sense of futuristic possibility, before speeding up and magnifying the eventual bust. History also suggests that recent technological changes may have a deeper impact, reshaping markets in the long run, too.

Economics and shifting alliances

One of the continuing themes of this newsletter will be that the shifting tectonic plates of geopolitics will bring about shifting alliances, deeper alliances and, in some cases, surprising shifts. The emerging geopolitics will not be the predictable game of chess that some commentators believe and understanding these alliances will be crucial for those looking to navigate geopolitical uncertainty.

The OPEC cut in oil production of this week is one such signal. Foreign Policy argues that this suggests that Saudi Arabia is “pursuing a non-aligned diplomatic strategy.” President Macron’s concept of the Grand Bouleversement (the great upheaval) is another signal. It was again emphasised in his interview this weekend where he argued that Europe should reduce dependency on the US. A revived Gaullism and a desire for European “sovereignty” makes the idea of simple, bipolar dynamics more complicated.

The tightening of Japan-India relations is also a development that has passed by largely unnoticed. As Nikkei-Asia point out, Japan is backing an ambitious “bullet train” development for India. This follows the signing of a number of agreements between the two countries over recent months. As The Economist point out, this has been driven both by a common understanding and a common fear of China.

On the flipside of this is the increasing economic and political closeness between Turkey and China. This was highlighted by recent partnerships between the two countries over electronic vehicles. As Zeyi Yang of the MIT Tech Review puts it:

In January, a Turkish newspaper reported that Alibaba is planning on investing more than $1 billion to build a data center and a logistics center in Turkey. Alibaba owns Turkey’s biggest e-commerce company, Trendyol, and its overseas shopping app AliExpress is often the most downloaded free app in Turkey’s Google Play store. Shein, another important Chinese player in the fast-fashion industry, has also started manufacturing in Turkey after producing exclusively in China for a decade… [Turkey] plays a strong role in Beijing’s Belt and Road Initiative, and that role has only strengthened since the start of the Russia-Ukraine war, which made railway logistics through Russia less dependable…But Turkey is also important because, sitting at the intersection of Europe and Asia, it can be an entry point for Chinese tech companies aiming to go into the European market.

These emerging alliances are important to monitor in the age of uncertainty. A shift from unipolarity will most likely not lead to a simple bipolarity. Businesses need to prepare for shifting alliances and a multipolar world.

Does American politics resemble pro-wrestling?

A fascinating (and disturbing) piece in the Atlantic this week about how American politics has increasingly come to resemble professional wrestling. It talks about Trump’s friendship with WWE supremo Vince McMahon.

The argument goes that the binary, polarised world of US politics is built on a hyper dramatic world where there are no shades of grey. The use of nicknames, the revelling in the hatred of opponents, the chants, the orchestrated drama of the rallies can arguably be traced back to the wrestling ring.

Millions of people love wrestling; millions more loathe it. Many people simply don’t know what to do with it. Although the symbiotic relationship between politics and wrestling goes back centuries, it is fair to say that Trump exploited WWE tools and tricks better than anyone who had come before him. TV networks once carried Trump’s campaign rallies live because of their sheer unpredictability. In January 2016, it wasn’t enough for Trump to kick protesters out of a Vermont rally; he directed security to “throw ’em out into the cold” and “confiscate their coats.”

I’m not 100% sure that the thesis is complete. But it’s a compelling one all the same. And arguably digging deeper into the polarising playbook isn’t what an already polarised country needs. Perhaps one of many reasons why Americans should consider rediscovering cricket!

The best foresight is regular foresight

There was a fascinating OECD note published last week, which discussed building strategic foresight into public policy making. It discussed three different types of foresight interventions:

Major surgery. “For an organisation facing a profound disruption or crisis; considering a significant change in direction; or tasked with a momentous decision.”

Periodic check-up. “Preventive work can include discussing a set of future scenarios from a previous exercise, reviewing early-warning indicators of future change, or stress-testing the current strategy against a set of megatrends from an outside source. This is the kind of regular foresight that takes place in Finland’s government, where different ministries and committees report to each other on their futures work.”

Making foresight a habit. Building it into everyday routines. By building foresight into what your team does every day, you limit the need for “major surgery” at a later date.

The key headline from the report is that “the best foresight” is both timely and regular. This is what Artemon’s Future Coach concept is designed to achieve.