Inflection Points 3: Ikea's Embrace of Scenario Planning & Inflection Points In Tech

Inflection Points 3: Ikea's Embrace of Scenario Planning & Inflection Points In Tech

Thanks a million for following the Substack and for sharing with others. Please do share with anyone you think might be interested.

As ever, drop me a line david@artemonstrategy.com - via Twitter at djskelton or at artemonstrategy . You can find me on Linked In here. The Artemon site is here.

David

Ikea’s Embrace of Foresight

There was a fascinating piece in the Financial Times on Friday, which really touched upon what we’re trying to do with Artemon Strategy. It discussed how IKEA have realised that old style forecasting, planning and budgeting is no longer fit for purpose in a world of complexity and uncertainty. Instead, they have started using Foresight capabilities, such as scenario planning, which are much more suitable to an age of uncertainty.

As I wrote last week, plans are only useful if you consider the uncertainty in which the plans unfold (otherwise you’ll fail the Tyson Test) and Foresight capabilities allow companies to consider these uncertainties. According to Jesper Brodin, the CEO of IKEA:

could not help but join with the chorus of those who said they missed the old times — when the world seemed relatively stable, trends were predictable and this could be translated into a more or less credible multiyear business plan.

He understands though that such nostalgia does not make business sense and that methodologies need to be adapted to reflect new realities. According to Brodin, the use of scenarios and forecasting is “teaching us agility in how we operate.”

It is not just the traditional variables of financial modelling such as inflation and consumer spending that have become harder to predict. The past few years have also provided some unexpected lessons on how business and society cope with shocks and uncertainty.

We established Artemon Strategy (site here) because we feel that Foresight capabilities will quickly become a fundamental element of business success in an age of uncertainty. As IKEA have noted, Foresight capabilities, such as scenario planning, enable businesses to anticipate what an uncertain future might mean for them, be agile enough to adapt and able to act quickly when anticipated scenarios occur. We’re strongly of the view that effective use of Foresight will soon become an essential ingredient of business success. I’d love to have a chat with you about why Foresight is so crucial and what this might mean for you. Please drop me a line david@artemonstrategy.com

What Are The Inflection Points In Tech?

As I’ve discussed over the first two Substacks, we are in the midst of an age of growing uncertainty, which has upended so many long-held assumptions. Geopolitical shifts, deglobalisation, growing protectionism and shifting global alliances are just a handful of examples of this rising tide of uncertainty.

The backdrop to much of the pace of change is the continuing advances in tech, which are continuing to change industries and accelerate already dizzying global change and uncertainty. And we are on the cusp of one of the most important technological leaps forward since the invention of the microchip. In 2011, Netscape founder, VC funder and first rate Tweeter, Marc Andreessen, sagely observed that “software is eating the world”, with traditional industries being transformed by tech.

Eleven years later even greater advances in tech are speeding up the transformation of whole industries and economies. But big tech itself is rushing to adjust to the scope and speed of the innovation - clear in the knowledge that the next wave of innovation, change and regulation could reshape the tech sector just as it reshapes other industries. The Inflection Points in tech during 2023 will be some of the forces that will be driving some of the change and uncertainty in the wider economy. Understanding these changes and staying ahead of them through Foresight capabilities will be essential.

Generative AI will continue to have plenty of WOW moments

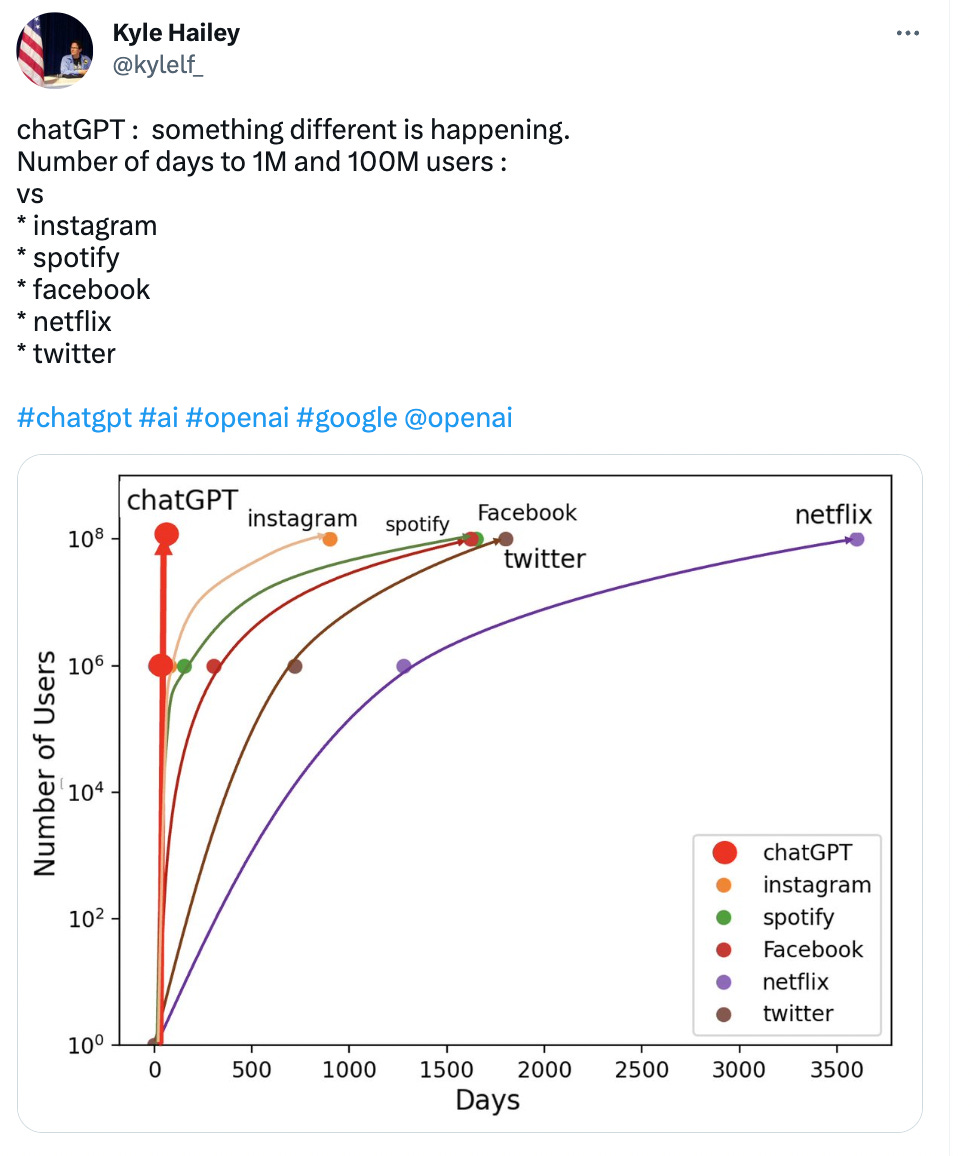

2022 was most certainly the year in which generative AI moved to primetime. AI has been fundamental to performance improvement across the product suite in Silicon Valley, but that improvement has been incremental and hasn’t resulted in any WOW moments. ChatGPT became the fastest growing launch in consumer history - compare its growth below to some of the most impressive recent examples.

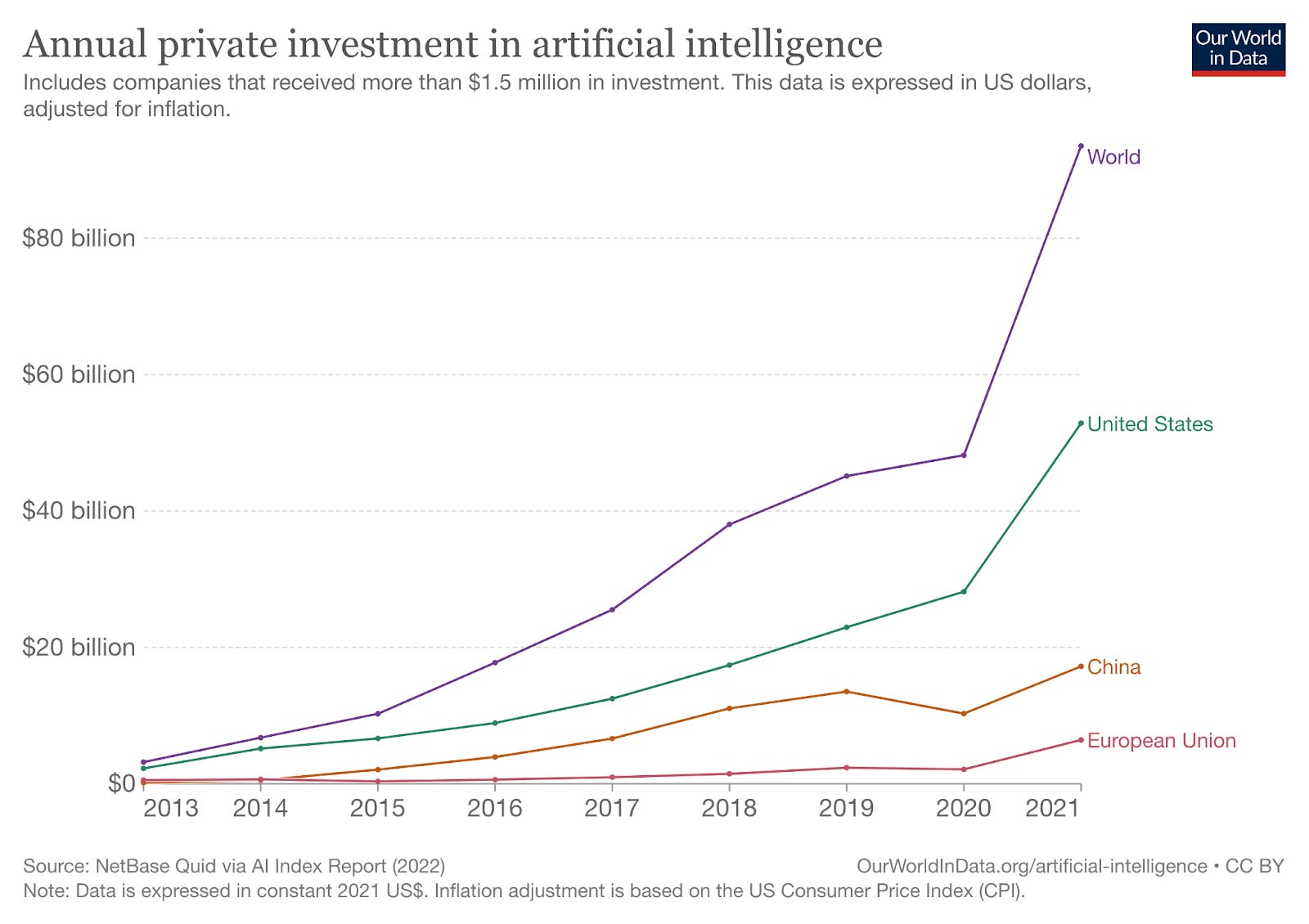

There was also an explosion in VC funding for AI last year, following on from a surge in investment since 2019.

AI will not only transform tech, but also bring huge benefits in traditional industries, such as manufacturing and agriculture and bring tremendous advance in healthcare. Bain’s Open AI Services Alliance is the kind of venture to note as AI’s application to the broader economy And as the technology improves, so will the WOW moments. Whether that’s enough to cause large-scale disruption in the short-term remains to be seen. Steve Jobs was correct when he said that successful disruption meant doing things multiple times notably better than the incumbent. It’s too early to tell whether that noticeable, multiple improved user experience will be brought about by the early wave of generative AI.

Generative AI will continue to have plenty of 😱 moments. This will make regulators nervous.

Chat GPT is undoubtedly enormously impressive, but its ability to mimic (please write an email in the style of…) and its speed have probably been more impressive than its accuracy. It all too often took on the role of an assertive, slightly drunken male in a bar - the ability to assert not always matched by the ability to be accurate. Rhiannon Williams noted the “confident bullshitter” problem when using AI to develop workout plans. SnapChat launched a ChatGPT powered chatbot last week with a health warning that “hallucinations” and “unexpected falsehoods” could be expected from the chatbot. Of course, large language models ultimately depend on the quality of the inputs and academics have already shown that high quality data will be exhausted by 2026, in contrast to low quality data, which will continue to be absorbed by 2030. A flood of generative AI could also risk a flood of material of varying accuracy and quality on the web, leading to a variety of challenges, including around indexing.

There are some side issues already emerging from generative AI. Some school boards have already shut off access to Chat GPT and I’d have thought that its rise will accelerate a return to pen and paper exams and the demise of coursework. Letting an AI chatbot loose has already seen it getting weirdly personal with a major tech reporter and describe Ben Thompson as a “bad researcher”. At a time when bad business speak (I still don’t think “learnings” is a real word) risks becomes ubiquitous, generative AI could overwhelm us with buzzwords and cliche. It’s a side point, but the cost of using AI in processing is expensive for tech firms - something that will undoubtedly be increasingly noticed as investors scour earnings reports.

The mimcry of generative AI is impressive, but the flipside of Spotify’s promise of a “realistic human voice” is neatly counterpointed by the revelation that AI has already been able to hack into bank’s voice based security systems. Realistic impersonation was one of the most notable characteristics of the AI hype in November and December and it doesn’t take too much of a stretch to see the journey from this to the potential deepfakes, fake news and disinformation have the potential to get worse. Stanford have already produced a masterly report about how advances in AI might impact influence operations, suggesting that generative AI raises the “prospect of highly scalable—and perhaps even highly persuasive—campaigns by those seeking to covertly influence public opinion.”

In such a rapidly changing environment, it’s essential to use Foresight capabilities to consider how AI might develop and impact on the wider business and governance environment. Generative AI has transformative positive potential, but ensuring its use is responsible, ethical and downsides are understood and acted upon is a business and C-suite issue, not a technologist issue.

A rare political consensus will continue to drive tech regulation. This might start to impact product development.

Generative AI going from geek to mainstream won’t escape the notice of regulators. It isn’t hard to see governments quickly getting nervous about scare stories. Even the CEO of Open AI described the worst-case scenario of generative AI as “lights out for all of us.” Every wave of dystopian scare stories risks producing a Dangerous Dogs Act style knee-jerk, which could be catastrophic for innovation.

We’re already seeing a wave of AI specific regulation. The FTC is warning against AI based “snake oil” and reminding companies to “keep their AI claims in check”. The EU have laid out the foundations for their approach based on levels of risk. The OECD AI Principles and the UNESCO AI Ethics represent a building block for “human-centric AI”, which might inform well-thought through legislation.

Generative AI is stepping into an environment where stronger tech regulation continues to be one of the few issues that will produce political consensus. Polarised American politics is brought together by the desire for some tech regulation. Europe continues to produce what it sees as hegemonic tech regulation. British political parties squabble about who can be the harshest on big tech. There’s a continuing wave of tech regulation in Asia, most notably of late in India and Indonesia.

The political consensus emerging around tech poses a bigger question - namely whether tech companies will consider potential regulation in product design and innovation and whether regulators might start considering the innovation life-cycle when designing regulation. As Nicklas Llundblad argues in this excellent thread, getting regulation right will need regulators and technologists to better understand the purpose of any regulation and what technology might look like within that paradigm. Ensuring that technologists and regulators better understand each other might produce better regulation and better technology.

A perfect storm of innovation, regulation, geopolitics and changing consumer preferences will continue to pressure business models

Previous periods of tech-driven flux have transformed a status quo that once seemed entrenched and permanent into an embattled ancien regime. Business models that once seemed immovable are now facing multiple challenges at the same time. Rapid waves of innovation and an increasing number of insurgents are already showing a willingness to take risks that established (and heavily scrutinised) players are unable or unwilling to take. But, as is the nature of perfect storms, after years of stability this is happening when shifting geopolitics, increasing regulation, rising scrutiny and increasing consumer expectations are increasing pressure on business models at the same time.

We know that transformative AI is being developed by emerging players and that EUREKA moment that changes everything could come from one of these insurgents. Just look at the sheer variety in the chart below:

The ability of insurgents to be able to ride the wave of emerging technology seems greater than it has been for decades, whilst bigger players are potentially held back by an understandable risk aversion and distracted by regulation and litigation. The challenge for bigger players is, of course, being able to be lean and innovative at the same time as kicking back against bureaucratic inertia and holding off emerging regulatory threats.

The digital advertising market will continue to fragment and business models continue to adapt

We’re probably in the middle of the first digital advertising recession (it was notable how robust digital advertising was in the aftermath of the 2008 banking crash). This has combined with the shuddering impact of Apple’s App Tracking Transparency (ATT), which caused a shuddering in some digital advertising markets. What once seemed a stable marketplace now seems volatile. The big two’s share of the market has continued to trend down, with more disruption seeming inevitable, including with the almost overnight emergence of new players in the space (look at the remarkable rise of Temu as an example).

Greater scrutiny being given to the so-called Attention Economy, most recently in this book from Tim Hwang, illustrates another increasing pressure being placed on the digital advertising model. An influential Wired article a few weeks ago also used a vivid description to talk about how platforms deteriorate when they pivot from user experience to chasing advertiser revenue. We’ve already seen both Twitter and Meta shift towards subscription based models and there continue to be rumours of news potentially being part of a separate (and higher) subscription cost.

As players who once relied on digital advertising seek to pivot towards subscription models and tech continues to work out what the rapid waves of AI mean for monetisation, we might well be in the midst of a dramatic change. Foresight is crucial to understanding how these various potential changes might play out.

The Splinternet Continues To Splinter

The Splinternet (the fracturing of the global internet) moved from emerging theory to reality in 2022. The splintering of the web has been happening for some time and digital globalisation has been receding from a high watermark through a period of techno-nationalism, stricter data controls and more vociferous appeals for digital sovereignty. Last year accelerated these anti-globalist waves and meant that, even within Europe, the free movement of information and data could not be taken for granted. Because of this, the annual state of the Open Internet report still makes for gloomy reading (with occasional bursts of Tiggerish optimism).

Authoritarian regimes increasingly see tech as a means of control, rather than empowerment and advances in AI technology potentially make dictators more dangerous. China is continuing to export authoritarian technologies and is sharing ways of limiting or controlling the global internet. Russia attempted to cut off the global internet and many other authoritarian regimes are increasing their attempts to severely limit access to information.

A splintered internet is a very different environment for companies to navigate compared to a frictionless global web. Using Foresight to anticipate how the environment for business might change further and how you should adapt is increasingly essential.

AI Spring? VR Autumn and driverless winter?

As noted above, the AI Winter seems to be very much be over, but it’s feeling pretty autumnal for VR and autonomous vehicles. Making condident predictions can be a difficult business and the 2016 prediction from Lyft’s founder that by 2021 most Lyft rides would be in autonomous cars and by 2025 personal car ownership would be a thing of the past hasn’t aged hugely well. If Silicon Valley is betting big on generative AI, the love affair with driverless seems to be waining. Traditional car manufacturers are stepping back from autonomous (see the decline of Argo AI) and tech firms are also feeling the pinch, both in Silicon Valley and in China. VC funding is down in autonomous vehicles and a Crunchbase analysis of 14 autonomous vehicle companies saw an average 81% decline in value since IPO. Similarly, despite the latest wave of VR hype and despite pretty well-sourced rumours of Apple being on the verge of a $1,000+ headset, the rest of VR seems pretty chilly. As Ben Evans noted this week, Meta is reducing the price of its QuestPro. Microsoft, Bytedance and Tencent are also cutting back their VR teams.

When The Trend Bends

This is an occasional feature that considers whether we might be at the beginning of a “bend” in various trends. Inspired by the concept that “a trend… is a trend… is a trend… until it bends.”

Ikea’s small format city centre stores, inspired by the belief that the “retail environment is changing.

After years of “demography as destiny” inevitability talk, red states in the US might be starting to swap economic places with blue states.

Spending on apps fell for the first time last year. Part of a change in consumer behaviour or a blip?

Is the podcast boom over?